Life has a funny way of throwing you curveballs, doesn’t it?

For most of my life, I lived comfortably without the burden of debt. But then - a third child, the decision to put them through private school, unexpected medical bills, and my wife’s sudden health issues leading to her inability to work - suddenly I found myself in unfamiliar territory. I had a car loan, a second mortgage, and the daunting task of figuring out how to pay it all off.

But, you know what? I learned a lot along the way. Now, I would like to share with you some tools and tips that helped me navigate through this journey. Before you get started paying off your debt, it’s crucial to choose a strategy that suits your financial situation. There are two popular methods to tackle this - the Snowball and Avalanche methods.

Payoff Methods

The Snowball method involves making minimum payments on all your debts save for the smallest one. You direct all the extra cash towards paying off this smallest debt first. Once that’s paid off, you roll the amount you were paying on that debt to the next smallest debt, and so on. This method is a great motivator as it provides quick wins.

On the other hand, the Avalanche method recommends making minimum payments on all debts, except the one with the highest interest rate. Any extra cash is directed towards this debt until it’s fully paid off. Then, you move onto the next highest interest rate debt. This method could save you more money over time since it tackles high-interest debts first.

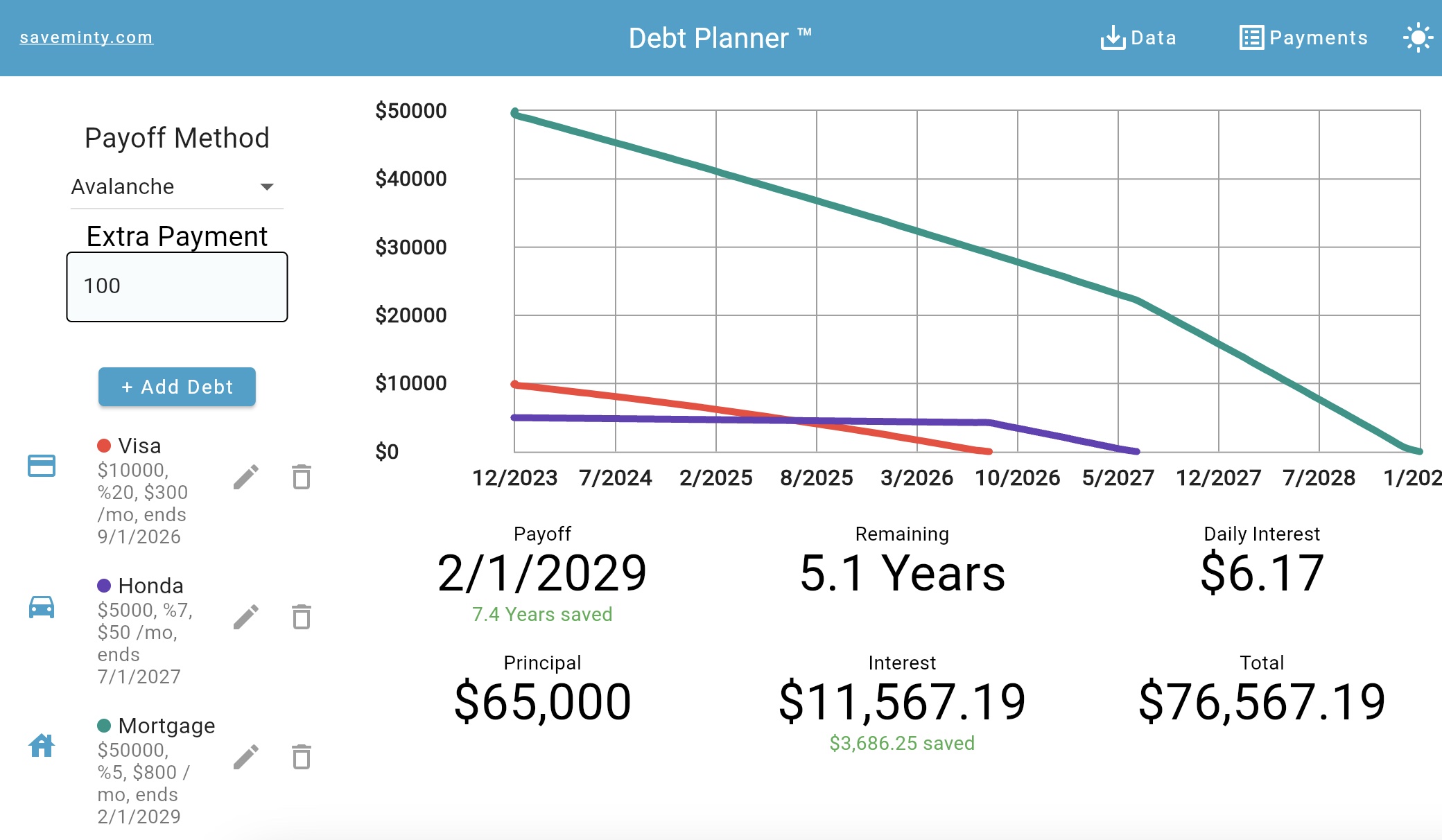

Figure 1. Debt Pay Off Calculator (https://www.saveminty.com/articles/debt-payoff-calculator)

Figure 1. Debt Pay Off Calculator (https://www.saveminty.com/articles/debt-payoff-calculator)

Choosing between these methods, Snowball or Avalanche, depends on what motivates you - quick wins or long-term savings. Fortunately, I have created a tool that lets you model your debt repayment using both methods so you can choose which is right for you: Debt Pay Off Calculator. The tool is completely free and requires no signup.

In my case, I took into account the principal payment and the overall payment amount. My car was a large payment amount being a short loan, and paying that off first meant that I could apply that cash flow towards other loans. Luckily, I did not have credit card debt. If you do, then you definitely want to pay that first before car loans or mortgages. See Debt Consolidation below.

Another important aspect of achieving debt payoff success is to create a budget and stick to it. This means tracking your expenses, identifying areas where you can cut back, and allocating a certain amount of money towards debt repayment each month.

Some General Tips

Analyze: Analyze your debt before you can begin to tackle your debt, you need to understand exactly what you owe and to whom. Begin by making a list of all your debts, including the balance, interest rate, and minimum monthly payment. Then, prioritize your debts by interest rate, paying off the highest interest rate debts first.

Budget: Create a budget now that you know how much you owe, it’s time to figure out how much you can realistically afford to pay each month. Take a look at your monthly income and expenses and cut back on any unnecessary expenses. Create a budget that includes debt payments and stick to it as much as possible.

Debt Consolidation: If you have multiple high-interest rate debts, it might be worth considering debt consolidation. This involves taking out a loan with a lower interest rate to pay off your higher interest rate debts. This can simplify your payments and help you save money on interest in the long run.

Increase Income: If you’re struggling to make your minimum monthly payments, consider finding ways to increase your income. Whether it’s getting a part-time job or selling items you no longer need, any extra income can help speed up your debt payoff journey.

Grit: Finally, the most important step is to stay committed to paying off your debt. This might mean making sacrifices, like avoiding eating out or shopping for non-essential items. But remember, the sacrifice is temporary and the long-term benefits of being debt-free are worth it.

Conclusion Paying off debt can be hard, but it’s not impossible. By following these steps, you can create a solid plan for paying off your debt and finally break free from its grip. Remember to stay committed to your plan and don’t get discouraged if it takes time. The important thing is to keep moving forward and celebrate each milestone along the way.

Finally, here are some more resources that are helpful for paying down debt: Other Resources

NOT FINANCIAL ADVICE

The information contained on this Website and the resources available for download through this website is not intended as, and shall not be understood or construed as, financial advice. I am not an attorney, accountant or financial advisor, nor am I holding myself out to be, and the information contained on this Website is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation.

I have done my best to ensure that the information provided on this Website and the resources available for download are accurate and provide valuable information. Regardless of anything to the contrary, nothing available on or through this Website should be understood as a recommendation that you should not consult with a financial professional to address your particular information. I expressly recommend that you seek advice from a professional.

I shall be held liable or responsible for any errors or omissions on this website or for any damage you may suffer as a result of failing to seek competent financial advice from a professional who is familiar with your situation.